Mapping Large Data Centres in Alberta

Exploring the AI datacenter boom in Alberta and tracing it’s possible impacts.

From the confluence of the Peace and Smoky rivers in the northwest to the drought-stricken plains of the Milk River basin, Alberta’s hydrocarbon heartland is becoming a proving ground for hyperscale compute. A deregulated power market, cool climate, abundant natural gas, and a deep industrial workforce have made the province unusually attractive to datacenter developers. The result is a pipeline of 19 tracked projects in various states of progress, representing nearly 18 GW of named compute capacity, an energy footprint larger than Alberta’s entire present electrical grid [S1-S5, S37-S52].

That scale, in concert with horror-stories from down south, is why the conversation has shifted so quickly to public anxiety. In a moment when every part of civic life seems touched by some aspect of the AI boom, Albertans are exceedingly concerned with what happens when the cloud needs land, water, power plants, pipelines, transmission upgrades, cooling systems, road access, and municipal approvals?

This article is an overview of the project landscape and the main categories of impact. The details deserve more than one pass and this article alone is likely inadequate for the task at hand. Utilities, water, air, noise, and local land-use politics each have their own regulatory framework, risks, and blind spots. Before getting into those deeper pieces, it helps to put the projects in one place.

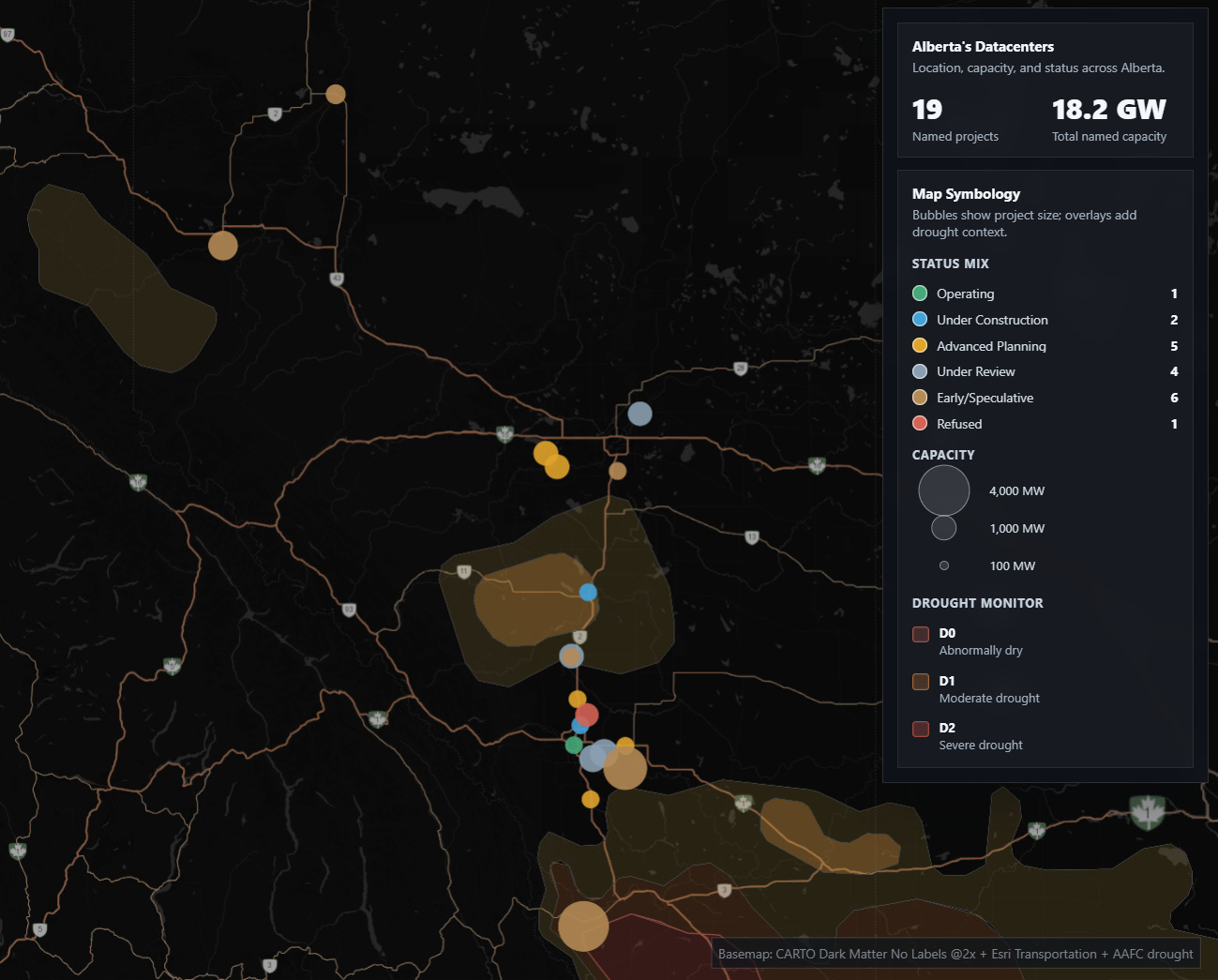

When and Where

The table makes two things clear. First, Alberta’s datacenter boom, unlike its industrial base, is surprisingly diverse. It includes operating cloud infrastructure, under-construction campuses, municipal applications, speculative announcements, refused proposals, and inactive legacy claims. Second, urgency and size often move on different timelines. A gigawatt claim signals ambition; power supply, water access, financing, and municipal acceptance are separate tests.

That distinction matters because the biggest bubbles are also the easiest to argue with. The 4,000 MW, 7,500 MW, and other province-bending claims make the map dramatic, and some may never see the light of day. The more immediate risks may come from smaller projects that are already operating, under construction, municipally approved, or far enough through planning to affect utility systems, water servicing, air emissions, noise, and local land-use decisions before the headline-grabbing pipe dreams become real.

Utilities and Grid

I come at this section with a bit of professional bias. I work in utilities planning, and I recently did some work connected to the City of Grande Prairie. When someone brought up a proposed datacenter in the region, I mentioned the estimated gas demand to a senior engineer. She audibly chortled. The reaction made sense: the number was absurd in the way only infrastructure numbers can be absurd, multiple times the gas demand of the entire city.

That is the first thing to understand about datacenters. Whether they connect to the NGTL system, a municipal gas utility, the electric transmission grid, or a private behind-the-fence power plant, these are massive loads. A 400 MW campus sits outside the scale of ordinary commercial development. A 1,000 MW campus is comparable to a major industrial load. A 7,500 MW announcement reads more like a regional energy strategy than a real-estate proposal.

Alberta’s first system-level constraint is the electricity grid. The Alberta Electric System Operator’s large-load process became the pressure valve for the boom, and the Large Load Integration Program separated projects that could connect quickly from those that would need longer study, system upgrades, or a new commercial framework. The Phase 1 allocation was limited and quickly absorbed by a small number of ready projects, leaving much of the pipeline exposed to Phase 2 rules and connection uncertainty [S3-S5].

Bill 8 changed the economics by pushing transmission upgrade costs toward the large loads that cause them [S7, S8]. That matters because connecting a datacenter can involve far more than a substation or line extension: broader network reinforcement, reliability modelling, and system planning. When those costs are assigned to the developer instead of spread across ratepayers, speculative projects become much harder to finance.

There is a potentially constructive version of this story. If large commercial consumers are going to place extraordinary demands on aging gas and electric systems, governments and utilities may be able to use those projects to offload some of the cost of building, reinforcing, and maintaining public infrastructure. In theory, that could reduce pressure on ordinary ratepayers by making the biggest new users pay for the capacity they require.

The harder question is whether the policy framework is precise enough to make that happen. If the rules are too loose, public systems can absorb hidden costs. If they are too rigid, credible projects may flee to private gas generation or avoid the grid altogether. The public interest sits in that narrow middle: capture infrastructure contributions from large users without creating a free-for-all of private utility islands.

The predictable response is the gas pivot. Projects that cannot wait for or afford the grid increasingly try to bring their own power through behind-the-fence generation, co-location with existing power plants, or fully self-supplied gas campuses [S8, S9, S18, S29]. That may reduce immediate pressure on the public grid while moving the public-interest question from transmission planning into power plant approvals, gas infrastructure, air emissions, noise, and land-use review.

The regulatory risk is fragmentation. A project can look manageable when each piece is reviewed separately: the load, the plant, the pipeline, the water licence, the subdivision, the development permit. The cumulative project is something larger.

Water

Water is the quiet constraint in the datacenter story, and it is also the part of this file where I want to be most careful. Utilities and emissions are closer to my professional lane. Water licensing, basin management, irrigation transfers, and drought policy sit outside it. This section is therefore a marker for deeper research and a placeholder for a fuller article.

Cooling design varies dramatically. Some facilities can rely on closed-loop liquid cooling or dry cooling. Others may use evaporative or hybrid systems that require more water. In northern or open-basin locations, that may be a manageable industrial servicing question. In southern Alberta, it becomes a basin-allocation question.

Much of the southern project geography touches the South Saskatchewan River Basin system, including the Bow, Oldman, and Red Deer basins. These basins are heavily allocated landscapes with municipalities, irrigation districts, farms, ecosystems, and drought exposure already competing for water. That is why the main figure includes the drought overlay: it lets the reader see that several proposed projects sit inside or near water-stressed regions, instead of treating location as a neutral dot on a base map [S21, S22, S23].

Closed-basin exposure rarely creates a simple yes-or-no answer; it changes the approval pathway. Developers may need to secure existing licences through private transfers, rely on municipal systems, or redesign cooling to reduce consumptive use. Under the Water Act, conservation holdbacks can become part of the transfer discussion, even where current policy makes those holdbacks discretionary instead of automatic [S21, S22, S23].

The public-policy question is cumulative stress. One water-light project may be manageable. A dozen large projects in or near closed basins, each seeking municipal supply, transfers, or groundwater access, raises a different question: who is tracking the total burden before the basin becomes the limiting factor?

This deserves its own article. The right treatment would need to look project by project at cooling technology, water source, basin status, municipal servicing assumptions, licence transfers, drought conditions, and the actual regulatory process under Alberta’s water law. For now, the map should be read as a warning that water may become one of the main siting constraints.

Air and Emissions

The air issue follows directly from the power issue, and carbon is only one part of it.

If datacenters cannot secure timely grid connections, many will try to generate power on site. In Alberta, that often means natural gas. The province has the gas supply, technical workforce, pipeline network, and regulatory experience to make gas-backed self-supply plausible. That is precisely why the model is spreading [S8, S18, S29].

Alberta’s renewable siting rules make that pathway even narrower. After the 2024 pause on new renewable approvals, the province announced restrictions on projects on prime agricultural land and new protections for “pristine viewscapes,” including wind-turbine buffer concepts that critics described as a soft moratorium on large parts of southern Alberta [S53]. For datacenters, that policy context matters: if new wind and solar development becomes harder to site near load, developers have a stronger incentive to lean on gas generation, existing gas plants, or backup-heavy hybrid systems.

Self-supply also changes the local air profile of the AI boom. A grid-connected facility may have indirect emissions through Alberta’s power mix. A self-supplied campus with hundreds of megawatts of gas generation has direct emissions at or near the project site. Depending on the configuration, that can mean nitrogen oxides, carbon monoxide, particulate concerns, greenhouse-gas compliance obligations, and local air-quality questions [S18, S24, S27-S30].

NOx, a major respiratory irritant, matters here because many of the proposed self-supply designs rely on reciprocating gas engines, gas turbines, or hybrid configurations that could become major point sources. The core concern is what repeated engine starts, steady gas generation, peaking behaviour, and nearby receptors mean for regional air quality. A rural site can make a project look less intrusive on a land-use map while still putting combustion equipment close to farms, acreages, or small towns.

Diesel backup is the other piece that needs more attention. Datacenters typically require backup generation for reliability, and those generators can be numerous even when they are framed as emergency-only equipment. Current air and emissions rules often treat standby equipment differently from primary generation, which makes sense for ordinary facilities. At hyperscale, the same treatment becomes more complicated because the backup fleet can be large enough to matter on its own. Testing, maintenance runs, emergency operation, and cumulative site design all deserve scrutiny.

The Technology Innovation and Emissions Reduction system becomes relevant once facilities cross reporting and compliance thresholds [S24, S30]. Modular buildouts complicate the picture. A developer can phase a project in smaller increments, propose multiple units, or start with a modest initial load while preserving a much larger full-buildout claim. That makes the first application less intimidating while leaving the cumulative emissions question for later [S27-S30].

There is a real tradeoff here. Behind-the-fence gas may make some projects more reliable and reduce the need for public grid upgrades. It may also create a new class of gas-fired digital infrastructure with localized NOx, diesel backup, and permitting questions that legacy rules were never built to evaluate at this scale.

Noise and Local Land Use

For nearby residents, sound may be the most immediate concern.

Datacenters are often described as low-impact industrial uses because they lack the obvious visual profile of refineries or mines. That framing misses the sensory reality of large cooling systems, backup generators, transformers, and reciprocating engines. Continuous fan noise, low-frequency hum, and engine vibration can travel across rural landscapes, especially at night.

Alberta Utilities Commission Rule 012 provides a noise framework, including low-frequency noise criteria [S19, S20]. The problem is that compliance and lived experience can diverge. A project can satisfy a technical test while still producing a broad, persistent hum that nearby residents experience as intrusive. This is particularly sensitive in agricultural and acreage areas, where people often moved precisely to avoid urban-industrial soundscapes.

This is where Benn Jordan’s public work on acoustics and low-frequency sound is useful as a plain-language reference point: he shows how sound can be measured, perceived, and politically disputed in ways that simple decibel readings can miss [S54, S55].

Municipal land-use approvals therefore become a major filter. Counties and towns are being asked to evaluate projects that combine datacenter buildings, substations, gas generation, water servicing, traffic, noise, emergency response, and long-term industrial land conversion. Rocky View County’s refusal of the Kineticor proposal showed that local councils can stop or reshape projects even when the provincial investment narrative is favourable [S49, S50].

The gist of the concern is that municipalities are being asked to handle novel infrastructure problems with legacy planning rules: old setback formulas, old noise assumptions, old utility-servicing categories, and approval processes built for more familiar industrial uses.

Conclusion

Alberta’s datacenter boom is best understood as industrial infrastructure.

The AI economy can sometimes seem weightless when the extant of our interaction with it is a polished UI window. On the ground, it has a footprint: megawatts, water licences, gas lines, air permits, noise models, roads, substations, land-use bylaws, and county hearings. The 19 projects tracked here are more than points on a map. They are tests of whether Alberta’s existing regulatory systems can absorb a new kind of industrial demand without scattering the risks across ratepayers, river basins, rural neighbours, and municipal governments.

This overview is only the start. Utilities and grid integration deserve their own article. Water deserves its own article. Air emissions and gas self-supply deserve their own article. Noise, local land use, and municipal capacity deserve their own article. Each impact has its own regulatory architecture, its own blind spots, and its own risks.

For now, the map tells the first story: Alberta has become one of the places where the AI boom is becoming physical. The next question is whether the province can make that buildout legible, accountable, and fair before the biggest bubbles become real.

Bibliography

S1. Amazon Web Services. “AWS Canada West (Calgary) Region Launch.” Dec. 2023. https://aws.amazon.com/about-aws/global-infrastructure/

S2. eStruxture Data Centers. “eStruxture Announces CoreWeave CAL-3.” May 2026. https://www.estruxture.com/estruxture-announces-coreweave-as-anchor-tenant/

S3. Alberta Electric System Operator. “Large Load Connection Queue Updates.” Oct. 2025.

https://www.aeso.ca/

S4. Alberta Electric System Operator. “Phase 1 LLIP Allocation Decisions.” Oct. 2025.

https://www.aeso.ca/

S5. Alberta Electric System Operator. “Large Load Integration Phase 2 Working Group.” Jan. 2026.

https://www.aeso.ca/

S6. Capital Power. “Q4 2025 Investor Presentation.” Late 2025.

https://www.capitalpower.com/

S7. Government of Alberta. “Bill 8: Utilities Statutes Amendment Act, 2025.” Dec. 2025.

https://www.assembly.ab.ca/

S8. Bennett Jones LLP. “Alberta Shifting Transmission System Upgrade Costs to Large Loads.” Dec. 2025.

https://www.bennettjones.com/

S9. Pembina Pipeline. “Greenlight Project Fact Sheet.” Late 2025.

https://pembina.com/

S11. Amazon Web Services / Leduc County. “Amazon Leduc County Solar Project.” Apr. 2021.

https://aws.amazon.com/

S12. Amazon Web Services / Vulcan. “Amazon Vulcan County Solar Project.” June 2021.

https://www.newswire.ca/

S14. Red Deer County. “Blindman Industrial Hub Approval.” Late 2025.

https://www.rdcounty.ca/

S15. Havenz Smart Communities. “Rolls-Royce Hydrogen Engines Arrive.” Jan. 2026.

https://havenz.ai/

S16. Alberta Utilities Commission. “AUC Rejection of Synapse Application.” Mar. 2026.

https://www.auc.ab.ca/

S17. Alberta Utilities Commission Proceeding Registry. “Synapse Re-submission.” Apr. 2026.

https://www.auc.ab.ca/

S18. Impact Assessment Agency of Canada. “Beacon Indus IAAC Registry #90121.” Late 2025. https://iaac-aeic.gc.ca/050/evaluations/proj/90121

S19. Alberta Utilities Commission. “Rule 012 Noise Control.” Late 2025.

https://www.auc.ab.ca/

S20. SLR Consulting. “Noise Assessment Briefing.” Early 2026.

https://www.slrconsulting.com/

S21. Government of Alberta. “Water Act Section 83 Transfer Rules.” Mid 2025.

https://www.alberta.ca/

S22. Alberta Environment and Protected Areas. “Water Transfer Policy Updates.” Apr. 2025.

https://watercanada.net/

S23. Government of Alberta. “Water Act, RSA 2000, c W-3.” 2000.

https://www.alberta.ca/

S24. Government of Alberta. “TIER Regulation Overview.” Late 2025.

https://www.alberta.ca/

S27. Government of Canada. “Physical Activities Regulations, SOR/2019-285.” 2019.

https://iaac-aeic.gc.ca/

S28. Impact Assessment Agency of Canada. “IAAC Project Description Project 90121.” Late 2025. https://iaac-aeic.gc.ca/050/evaluations/proj/90121

S29. Impact Assessment Agency of Canada. “IAAC Registry Project 89901.” Mar. 2026. https://iaac-aeic.gc.ca/050/evaluations/proj/89901

S30. Government of Alberta. “Technology Innovation and Emissions Reduction Regulation.” 2019.

https://www.alberta.ca/

S31. Rocky View County. “Wild Rose Power Hub Area Structure Plan Application PL-2025-0012.” 2025.

https://www.rockyview.ca/

S32. Rocky View County. “Wild Rose Power Hub Public Hearing Notice.”

It could be worth some discussion as to the size at which data centres become problematic. Are we just worried about hyper scale data centres with their own power plants? For example, there are a number of smaller data centres already operating for years in Edmonton and Calgary (e.g https://www.datacentermap.com/canada/edmonton/). You could also add Bitdeer’s 100MW facility that just started construction in Fox Creek. That one’s actually a bitcoin mine, which raises another interesting topic as to whether certain uses are more acceptable than others (with bitcoin mines probably being at the parasite end of the spectrum). And if they’re using ASIC miners they’re not actually that adaptable to other data centre tasks.